Real Estate as an Asset Class

Published May 2013

Written by Shawn Yap CFP

Real estate is one of the major asset classes among bonds, cash and equities in an investment portfolio. Other asset classes may include commodities, currencies, derivatives, alternatives, etc. The purpose of diversification is to reduce volatility (risk) because different asset classes perform differently under different market conditions.

There are many ways to invest in real estate. The easier ways are through real estate company stocks, Real Estate Investment Trusts (REITs) and unit trusts. They are easy because of the low entry requirements starting from as low as a few thousand dollars with ease of withdrawal. The other way is to purchase real estate directly either on your own or jointly with others. Compared to paper assets, direct real estate, being tangible, has always had the alluring nature in the sense that you can see it, touch it, feel it and even smell it. However, this method requires more knowledge and skill just like investing directly in stocks on your own where you need to look at company statements, valuations, fundamental and technical analysis. In direct real estate investment, purchase price, interest rate & rental rate are some of the key factors that affect potential capital growth and income yield.

Capital Growth

One of the key advantages of direct real estate investment is the power of leverage. Say in 2009 (market bottom which nobody would have known), you have $100,000 to invest. You have 2 choices: One is to invest in the stock market and the other is to purchase a $500,000 property with $100,000 as a down payment. Assuming both the stock and property markets recovered and doubled in value, you would have made $100,000 from the stock market versus $500,000 from the property. Even if your property value increases by only 50% while the stock market doubled, your gain of $250,000 would still be 250% more than your stock gain. For property flippers, the gain would have been compounded higher. This may sound easy and exciting but it relies heavily on the often challenging task of purchasing at the bottom part of the property cycle. Imagine you buy a $1 million property today with a 20% downpayment and the next thing you know, your property value drops 30% to $700,000. This negative equity situation means that in addition to losing your $200,000 downpayment, you still owe the bank $100,000. Leverage works both ways. Unlike paper assets, a real estate investment is considered illiquidity. You cannot exchange it for cash in a week, and selling it in a bad market will escalate your losses.

Of course, real estate is for long term but how long is long? Well, research has shown that if you bought at the peak of the property cycle prior to the Asian Financial Crisis, it could take as long as 15 years just to break even.

Income Yield

There are many ways to measure yield. The most common is called Gross Yield, obtained simply by taking the yearly rental amount divided by the purchase price. However, this is too simplistic and insufficient to assess the real rate of return. Take for example a $1 million residential property with a $200,000 downpayment.

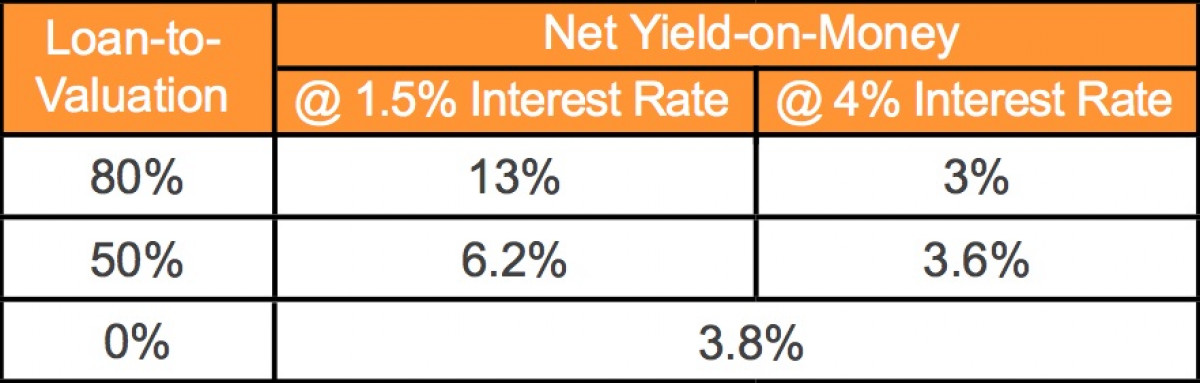

Assuming that the yearly gross rental is $48,000, the Gross Yield will be 4.8% ($48,000/$1,000,000). If we take into account the maintenance costs and taxes (assume $10,000 per year), the Net Yield will be 3.8%. This is a 20% difference in yield. For some property investors, they may use Yield-on-Money. Instead of using the property price as the denominator, they use the downpayment which is their actual capital outlay. In this case, the Yield- on-Money is 19% ($38,000/$200,000). So far, you would have realised that the mortgage repayment is not taken into consideration. Assuming that a loan-to-valuation of 80% is taken over 30 years with a mortgage interest of 1.5%, the yearly instalment is about $33,000 of which $12,000 is interest. Taking the interest payment as a cost of investment, the Net Yield-on-Money comes to 13% ($26,000/$200,000). For this example, this property provides a positive cashflow of $5,000 per year ($48,000- $10,000-$33,000). Unless you think that mortgage interest rate would remain at 1.5% in the next 30 years, a prudent rate of about 4% (historic average) should be used for evaluation. If mortgage interest rate increases to 4%, the Net Yield-on-Money reduces to just 3% with a negative cashflow of $8,000 per year for the investor.

The table below illustrates the different permutations:

Other Considerations

Other than interest rate risk, both rental rate and the availability of tenants are not guaranteed. It is prudent to keep a buffer of 1 to 3 months’ of rental for financed property in case the property is unoccupied especially in between contracts.

If you are investing with others, the type of ownership matters a lot. On the demise of any joint owner in a joint tenancy, the remaining owner(s) automatically take over ownership legally. A tenancy-in-common is usually used for investment properties as the ownership is retained in the deceased estate.

In addition to following the number one rule in real estate “location, location, location”, your knowledge on tenant profiles, rental demand and the macro view of the economy could add value to your homework. You can read extensively, attend seminars or seek the views of trusted real estate advisers in the quest for your brick and mortar investment.

This article first appeared in the May 2013 issue of Financial Planning magazine published by the Financial Planning Association of Singapore (FPAS).